Nowadays, buying a home for the first time can seem so difficult that it should be considered an Olympic event. It’s not just the paperwork that’s daunting, either; it’s the terminology, fees, and number of people involved. In the spirit of spreading valuable information to demystify some of the processes, The Mike McCann Team is here to help explain what you should be aware of when looking to buy a home in Philadelphia.

What Is a First-Time Home Buyer Loan?

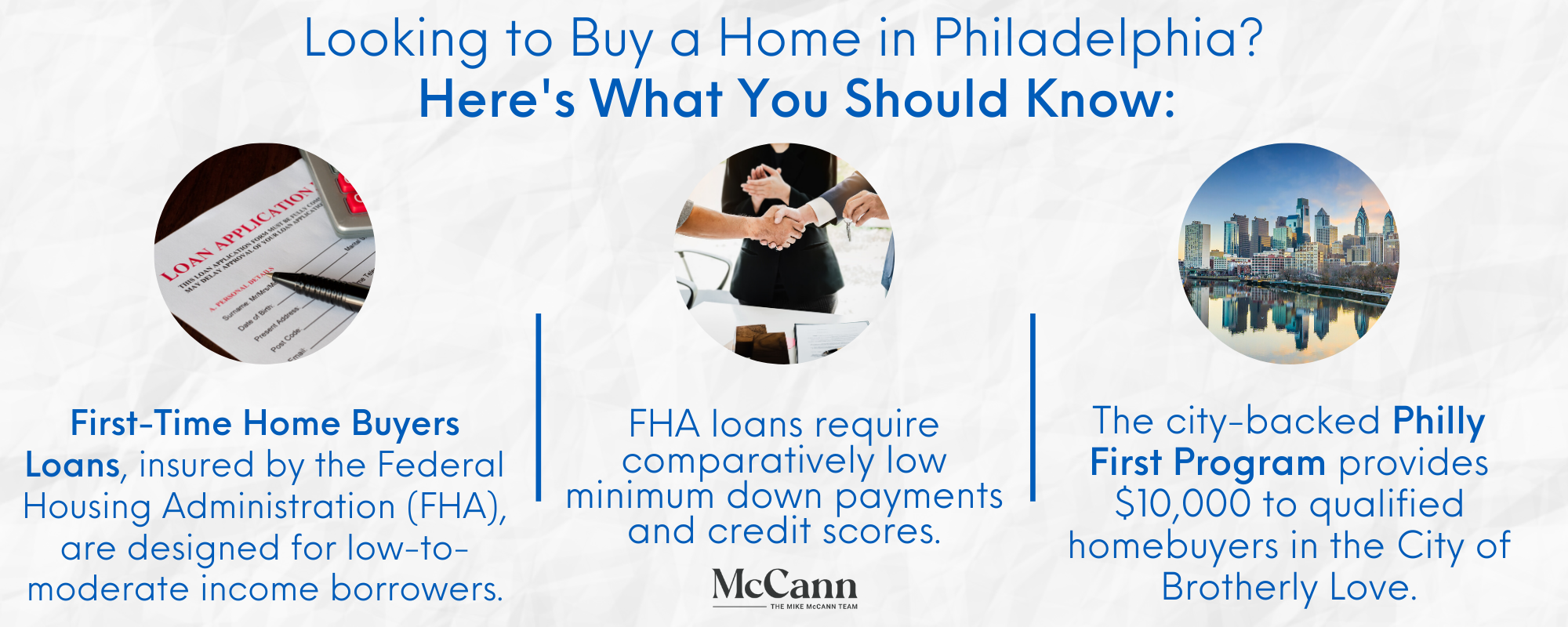

Simply put, an FHA mortgage is a home loan backed by the government and insured by the Federal Housing Administration. While they come with monthly mortgage insurance premiums, the lending requirements tend to be more flexible than a conventional loan. The qualification process is typically a bit easier, too. That said, if you’re looking for a home and need a loan with a comparatively forgiving credit requirement and a low down payment, an FHA loan may be right for you.

Does An FHA Loan Really Only Apply to My First Home?

Contrary to popular belief, FHA mortgages are not exclusive to first-time homebuyers. However, there are a few requirements to keep in mind:

- You must be able to prove United States residency and have a valid Social Security number

- The home in question must be your primary residence

- You must have a steady employment history or been employed at the same job for two years.

- The home must be a single-family unit, although it is not just limited to houses. Condominiums, townhomes, and duplexes may be eligible, as well.

- Must have a credit score no less than 580 (to qualify for the required 3.5 percent down payment. Buyers with lower credit scores will be required to put down more.)

Even if you have had a recent bankruptcy or foreclosure, you could still be eligible for an FHA loan in certain circumstances. They are subject to loan amount limits that depend on your geographic area.

So…What’s the Catch?

An FHA’s less stringent requirements don’t come entirely free, of course. Borrowers will need to pay FHA mortgage insurance. This is paid in two ways — upfront as a part of your closing costs, and then as part of your monthly payment. The upfront cost is 1.75% of your total loan amount, while the monthly cost varies based on the down payment amount, length of your loans, and initial loan-to-value (LTV) ratio.

Philadelphia’s Housing Development Grant

In May of 2019, Philadelphia city officials, the Division of Housing and Community Development (DHCD), and community leaders announced the Philly First Home program with expanded down payment assistance of up to $10,000 (or 6% of the home’s purchase price, whichever is lower). This program was designed to facilitate neighborhood sustainability in the City of Brotherly Love by making homeownership a more affordable, feasible reality. These funds can be used towards a down payment or closing costs.

Homebuyers must meet the following criteria to qualify:

- The home must be in the city of Philadelphia

- Must be a first-time homebuyer (or a buyer who has not owned a home for at least three years)

- Complete housing counseling

- Have a household income at or below 120% Area Median Income (AMI)

- The financial assistance provided by the city will become a lien on the property’s first mortgage.

For more information about affordable housing options, whether it’s your first time buying a home or not, contact Philadelphia’s top real estate agents today!